Most employees struggle to grow their 401k effectively. The IRS increased the 2026 401k contribution limits to $24,500 recently. This $1,000 jump from last year helps your money grow faster over time.

Many companies now use 401k auto-enrollment because of SECURE 2.0 rules. This employer-sponsored retirement plan gives you a head start on your future. You should check your settings to ensure you get your full employer 401k match.

This guide explains the basics of your 401k. We want you to understand the new rules and how they affect your paycheck.

What Is a 401(k)? Definition, Types, and 2026 401k Basics

Understanding your 401k helps you build wealth faster. These accounts offer specific 401k tax benefits that most standard savings accounts lack. Here is the breakdown of how these plans function today.

1. The Core Definition of a 401(k)

A 401k is an employer-sponsored retirement plan that lets you invest a portion of your salary directly from your paycheck. This system automates your savings and often reduces your tax bill.

Your employer provides a list of 401k investment options, such as index funds or target-date funds, to help your money grow. Because of SECURE 2.0, many new plans now include 401k auto-enrollment, making it easier to start saving without extra paperwork.

2. Traditional 401(k) vs. Roth 401(k): What Employees Need to Know in 2026

Choosing between a traditional 401k and a Roth 401k depends on when you want to pay taxes.

Traditional 401k: You contribute pre-tax dollars. This lowers your taxable income now, but you pay taxes when you take the money out later.

Roth 401k: You pay taxes on the money before it goes into the account. In exchange, your withdrawals in retirement are completely tax-free.

A new 2026 rule requires high earners who made over $150,000 last year to put their catch-up contributions into a Roth account. Both plan types follow the same 401k contribution limits, so your choice mostly affects your tax strategy.

Once you pick your plan type, you can focus on hitting the right contribution numbers to get your full employer 401k match.

How Do 401k contribution limits and employer 401k match Work in 2026

Maximizing your 401k requires knowing the exact numbers the IRS sets. For 2026, the 401k contribution limits have increased to help you build a stronger employer-sponsored retirement plan.

Staying informed ensures you get the most out of your 401k investment options.

1. 2026 401(k) Contribution Limits: What Employees and HR Professionals Need to Know

The IRS updated the 401k contribution limits to $24,500. This $1,000 increase over last year allows your account to grow faster. If you are older, SECURE 2.0 provides higher catch-up contributions for your retirement goals.

Standard Limit: $24,500.

Combined Limit: $72,000 (total from all sources).

Age 50–59/64+: An extra $8,000, bringing your total to $32,500.

Super Catch-up (Age 60–63): $11,250 extra, meaning a $35,750 deferral.

You must manually update payroll settings to reach these new goals, as systems often stick to old caps. Following these rules helps you maximize your 401k balance effectively.

2. How the Employer 401(k) Match Works

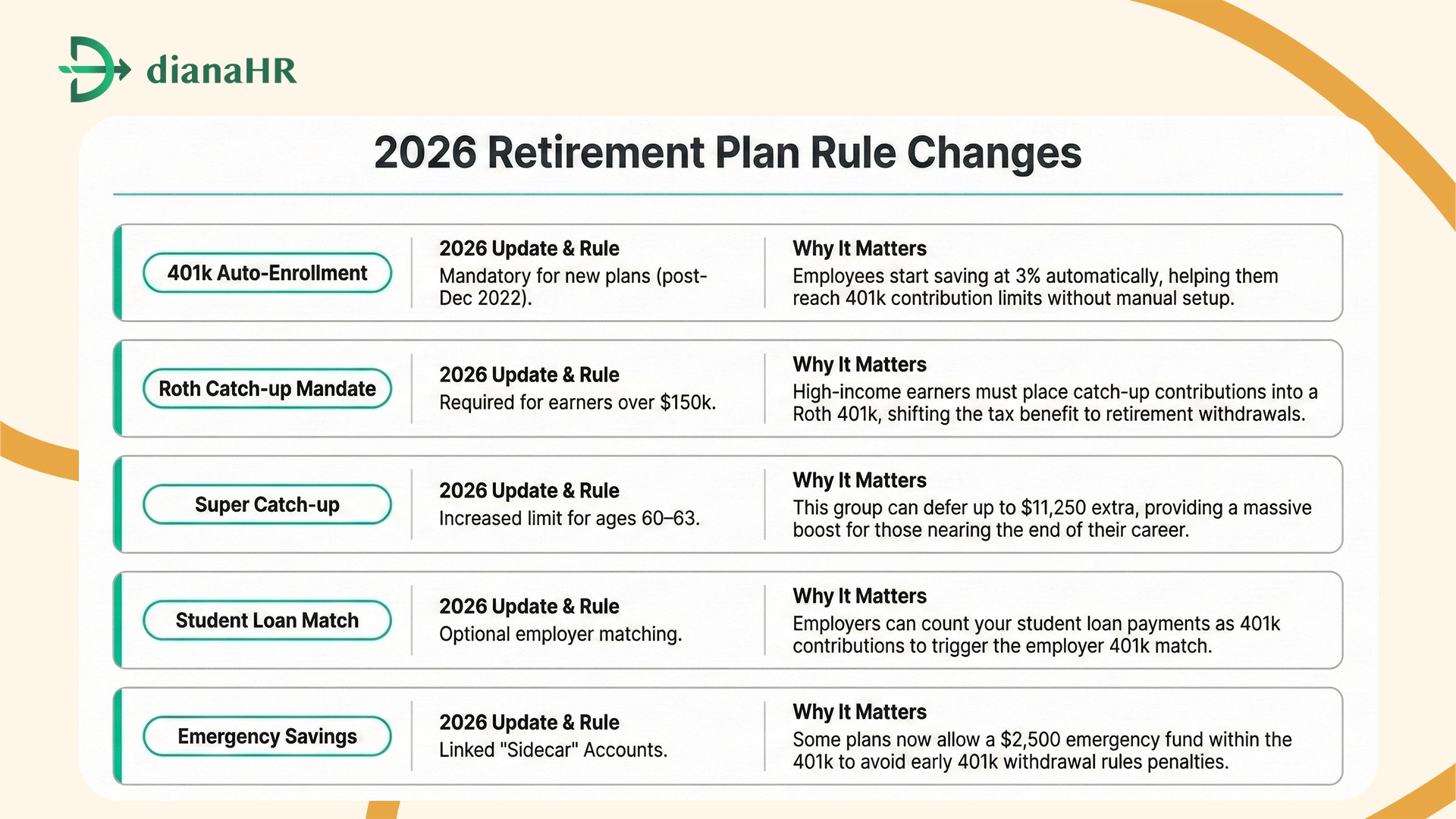

The employer 401k match is free money added to your account. Most companies match around 4% of your pay. A common formula gives you a full match on the first 3% and a partial match on the next 2%.

This employer 401k match does not count against your $24,500 personal limit. Failing to contribute enough to get the full match is a common mistake that limits your 401k tax benefits.

3. Vesting Schedules: When Employer Contributions Actually Become Yours

While money in your traditional 401k or Roth 401k is yours, the employer match follows a vesting schedule.

Immediate Vesting: You own the match right away.

Cliff Vesting: You own 100% after a few years.

Graded Vesting: Your ownership grows over time.

Before you consider 401k withdrawal rules, check your vesting schedule. Leaving too early means you lose unvested money. Many plans now use 401k auto-enrollment, which puts your money into a 401k automatically, but you still need to monitor your progress to maximize the 401k over time.

These limits and matches are the engine of your savings. Understanding them prepares you for more technical plan updates.

What SECURE 2.0 Changed About 401k Plans(Key 2026 Updates)

The SECURE 2.0 Act introduces major shifts for your 401k this year. Most new plans must now include 401k auto-enrollment, starting employees at a 3% savings rate. This change helps more people build an employer-sponsored retirement plan without taking manual steps.

1. Auto-Enrollment Is Now Required for New Plans

New businesses starting after late 2022 must use 401k auto-enrollment features. This ensures you start saving early, even if you forget to sign up. These rules push participation rates higher, helping you reach your 401k contribution limits through steady, automatic growth.

2. The Super Catch-Up Provision and Roth Catch-Up Rule

Two major 2026 changes specifically target older employees and high earners.

Super Catch-up (ages 60–63): You can now contribute a higher catch-up contributions amount of $11,250. This allows you to reach a total 401k deferral of $35,750 for the year.

Roth Requirement for High Earners: Beginning January 1, 2026, if you earned more than $150,000 in the previous year, the law requires your catch-up contributions to go into a Roth 401k. You can no longer use a traditional 401k for these extra funds.

These updates mean your 401k tax benefits might look different this year. Your company must offer a Roth 401k option to allow these extra savings for high earners. Tracking these changes ensures you still qualify for the full employer 401k match.

Key SECURE 2.0 401(k) Changes at a Glance:

How DianaHR Keeps Your 401k Compliance Automated

DianaHR automates your 401k tasks to save you 20 hours weekly. Our AI platform handles 401k contribution limits and syncs with payroll to stop errors. We track your employer 401k match to ensure every dollar stays accurate across all states.

Smart Compliance: We manage SECURE 2.0 rules, including 401k auto-enrollment and the 2026 Roth 401k catch-up mandates.

Expert Support: A dedicated specialist oversees your vesting schedule and plan policies.

Easy Integration: We work with ADP and Gusto to manage catch-up contributions without tool migration.

DianaHR reduces HR costs by 60% while keeping your employer-sponsored retirement plan simple and compliant. Our technology handles the heavy lifting so you can focus on growing your business.

Conclusion

A 401k is your strongest tool for building wealth. However, manual tracking often leads to missed 401k contribution limits or incorrect employer 401k match calculations.

With SECURE 2.0 bringing new Roth 401k rules in 2026, one small payroll error can trigger heavy IRS penalties and double taxation. These mistakes frustrate employees and put your business at risk.

DianaHR solves this by automating your employer-sponsored retirement plan tasks. Our platform syncs your payroll and benefits to ensure total compliance.

Book a DianaHR demo today to simplify your plan administration and protect your team’s future.

FAQs

1. What is the 401(k) contribution limit for 2026?

The 2026 401k contribution limits are $24,500 for individuals. If you are 50+, standard catch-up contributions reach $32,500. Those aged 60–63 can use the SECURE 2.0 super catch-up to hit $35,750. These updates help maximize your employer-sponsored retirement plan.

2. How does the employer 401(k) match work?

Your employer 401k match is additional money paid into your account based on your deferrals. Most companies match around 4% of your salary. This match helps you grow your 401k balance faster without counting toward your individual $24,500 limit.

3. What is vesting in a 401(k) and why does it matter?

Vesting determines when you own the employer 401k match. Your own money is always yours, but employer funds follow a vesting schedule. Understanding this is vital before you consider any 401k withdrawal rules or decide to change your job.

4. What changed about 401(k) plans in 2026 under SECURE 2.0?

SECURE 2.0 now mandates 401k auto-enrollment for new plans to boost participation. Additionally, high earners must now place catch-up contributions into a Roth 401k. These updates ensure your employer-sponsored retirement plan stays current with new federal laws.

5. What is the difference between a traditional 401(k) and a Roth 401(k)?

A traditional 401k uses pre-tax dollars to lower your current taxes. A Roth 401k uses after-tax dollars for tax-free withdrawals later. Both follow the same 401k contribution limits, giving you flexible 401k tax benefits based on your future income needs.

6. What happens to my 401(k) if I leave my employer?

You keep all your contributions and any vested employer 401k match. You can roll the balance into a new employer-sponsored retirement plan or an IRA. This move avoids taxes and early 401k withdrawal rules penalties that apply to cash payouts.

Share the Blog on: